It has also taught the mortgage industry a few things about the importance of effective automation, information security and integrity, contingency planning and customer communication.

From what it takes to accommodate remote notarization to figuring out how to process an influx of forbearance requests through limited communication channels, here are five takeaways from coronavirus-related work restrictions.

“While the technology components necessary for a fully electronic closing have been built by various companies that support the mortgage industry, my impression is that a relatively small percentage of mortgages industry-wide actually go through that fully electronic process,” said PK Parekh, senior vice president and business head at Discover Home Loans. “That’s because there is a complex web of county, state, agency, and investor requirements that make it difficult for many lenders to scale up a simple, uniform process for all of their customers.”

Ultimately, social distancing may make things like remote notarization more common, but not overnight. It can take upwards of 30, 60 or 90 days to install the remote notarization technology components because of multiple systems, parties and methods involved, said Craig Focardi, senior analyst, banking, at Celent.

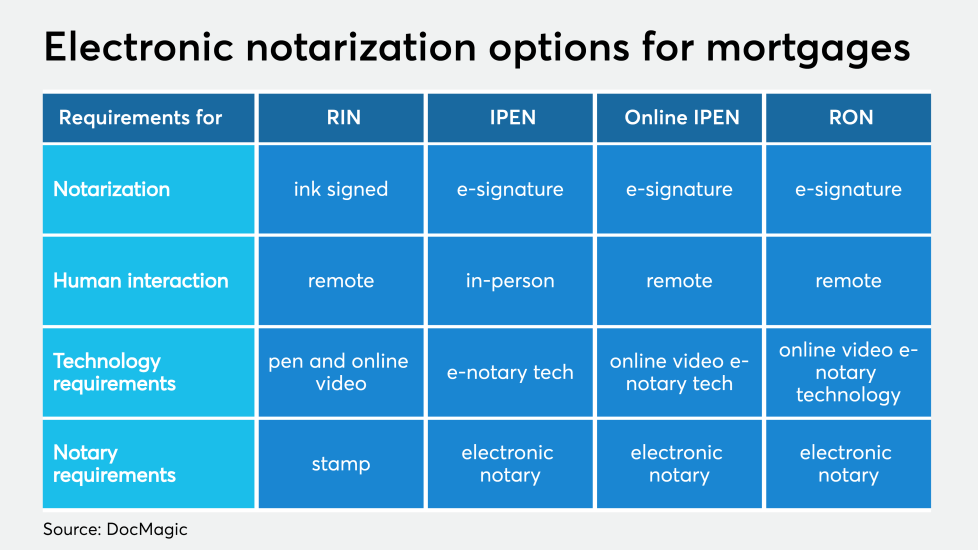

For example, different forms of remote notarization are used depending on what local rules and capabilities allow. These include remote ink-signed notarizations (RIN), remote online notarization (RON), in-person electronic notarization and online IPEN.

Companies have been able to operate without the technology, but may work more efficiently with it. Discover Home Loans, for example, reduced closed-end home-equity loan origination costs by more than 50%, notary errors by 46% and processing times by more than 30%, according to a Celent case study based on the lender’s experience implementing electronic closing and recording technologies from DocuTech and Simplifile last year.

“Virtually all mortgages can get closed today, but there’s a huge disparity in the level of effort and security between remote closing and notarization, versus when consumers have to drive to get to a closing, particularly in an environment where many banks are closing branches,” Focardi said.

“Cybersecurity has been a growing problem in our industry and a lot of what we do is with third-party providers,” said Regina Lowrie, CEO of risk management firm Dytrix. “Couple that with employees working at home and the issues associated with data privacy and cybersecurity become a bigger issue.”

One strategy for reducing wire fraud risk — even though it may seem counterintuitive in a remote work setting — is to minimize online communication related to closings. The more online data there is, the more likely hackers can get information that will help them perpetrate fraud.

“Try to reduce or eliminate any email traffic with the closing agent,” Lowrie suggests.

Lowrie also suggests companies review their warehouse lending covenants and cybersecurity insurance contracts so they know how much potential exposure they have to this risk. Cybersecurity policies tend to have an exclusion for situations where a staff member wires funds to a fraudulent recipient without taking steps to ensure those funds were going to the correct one, she said. Warehouse lending contracts are less consistent.

Money lost through wire fraud is rarely recoverable and incidents are common in the real estate industry, according to Lowrie. Losses from real estate and rental fraud in general totaled more than $200 million last year, according to the Federal Bureau of Investigation’s Internet Crime Complaint Center.

With the coronavirus expected to introduce more valuation fraud and underwriting risk into the market, mortgage companies are finding that they need ensure that remote appraisals provide a reliable estimate of collateral housing values as well as a safe one.

Some firms, like valuations and technology vendor Clear Capital, are looking to give clients the capability to do 360-degree scans of their homes, in place of a traditional walk-through. But simpler tools must suffice for now.

“Most people have a smart phone with a good camera so this is the lowest-friction way to do this right now,” said Kenon Chen, executive vice president at Clear Capital.

The dynamics of the job market within the mortgage industry could drastically change if remote work and other COVID-era contingencies are adopted permanently. The benefits of becoming a mortgage broker, for example, may look different in the post-pandemic period. Also, mortgage bankers and brokers may no longer be bound to working for firms in their immediate area.

It may be too soon to see how all that shakes out given the many uncertainties associated with the coronavirus implications and related government policies, but one thing is clear, the context mortgage professionals have to consider when looking at current tax implications of remote work is different now.

In some cases, however, mortgage companies are finding it more advantageous to engage their customers through multiple communication channels, and speak with them in more detail.

“When customers inform us they have been impacted by COVID-19 and would like a forbearance, we provide it to them,” said Mike Dubeck, CEO and president of Planet Home Financial Group. “And when we speak with customers, we are taking more time to explain the nuances in the options available to them.”

For example, a customer may not realize the options they have for repaying the debt later. Laying out all the options and answering all their questions can help, Dubeck said.